INTRODUCTION

Tobacco use continues to threaten public health as a leading cause of preventable morbidity and mortality worldwide1. In an effort to address the global burden of tobacco use, following the adoption of the World Health Organization (WHO) Framework Convention on Tobacco Control (FCTC), the first international health treaty2, the WHO established six MPOWER measures to help countries implement effective interventions proven to reduce tobacco demand2. These measures include: Monitor tobacco use and prevention policies; Protect people from tobacco smoke; Offer help to quit tobacco use; Warn about the dangers of tobacco and anti-tobacco mass media campaigns; Enforce bans on tobacco advertising, promotion and sponsorship; and Raise taxes on tobacco.

With countries making progress towards implementing these tobacco control measures3, the tobacco industry has responded in new ways to promote their products. Innovation has emerged as a key marketing strategy of transnational tobacco companies4. Historically, the tobacco industry has added flavorings, including the most common flavor menthol, to tobacco products5. Evidence suggests that flavors encourage smoking initiation and progression to regular use, particularly through their role in increasing palatability and appeal of tobacco5–8. Moreover, menthol’s cooling and anesthetic properties can reduce the harshness of tobacco smoke on the throat, thereby facilitating inhalation5. Tobacco industry marketing of MNCCs to various targeted populations, such as adolescents, females, and racial/ethnic and sexual minority groups, is well documented5,9,10. More recently, since 2007, flavor capsule cigarettes (FCCs), which contain one or more capsules in the filter that release flavoring when crushed by the consumer, have entered the market11. Advertised by the tobacco industry as being technologically advanced, offering consumer choice/ customization and a unique sensory experience, FCCs have gained popularity globally. In some countries FCCs only come in menthol flavor, while in others a plethora of flavors are available on the market12. While there is overlap in these product groups, global market trends may differ between MNCCs and FCCs.

Monitoring global tobacco use, including surveillance of market trends, is critical for identifying needs and priority areas for increased tobacco prevention and control strategies, and aligns with the M of the MPOWER measures (Monitor). However, studies examining MNCC market data are largely concentrated in specific countries, such as the United States13-15, Australia16, and Singapore17. Global data on MNCC market shares are limited and/or outdated. The most comprehensive global study on MNCC market shares, which covers 55 countries, dates back to 200118. Some studies have used the commercial database Euromonitor Passport to explore short-term trends in global market shares of FCCs. These have highlighted that the largest FCC markets are in Latin American countries, including Peru, Guatemala, Mexico, and Argentina, where market shares increased by at least 40% between 2014 and 201711,19. Another study presents Euromonitor data on combined market shares of MNCCs and FCCs, across the UK and the EU member states, and other countries in the WHO Europe Region, demonstrating a growth in sales from 2004 to 2018. The EU, however, has shown a downward trend from 2015, after the EU/UK characterizing flavor ban was announced20. Another study examined combined menthol and capsule cigarette market trends by country income level using Euromonitor data21. This study found market growth from 2005 to 2019 in both upper middle-income (4.0% to 12.3%) and lower middle-income (2.5% to 6.5%) countries (with no market data for low-income countries)21. While they are important studies, they do not provide comprehensive global coverage and/or do not address potential differences in market shares of FCCs and MNCCs.

Several studies have examined individual-level correlates of MNCC and FCC use. Younger age and being female are consistently associated with use of both across many countries, while other characteristics, such as socioeconomic status, race/ethnicity, and living in rural areas, generally vary by country or findings are mixed5,18,22-25. Little is known, however, about country-level factors that may be related to greater use of these products in some countries over others. Studies suggest that tobacco industry marketing plays a large role in the population use of MNCCs as well as FCCs12,26. It is possible, though, that other country-level factors, including policy-related factors, may be driving market share differences. Ecological analyses can provide such insight and may inform tobacco control strategies. Previous studies have examined ecological factors, such as socio-economic factors (Gross Domestic Product27, unemployment rate27,28), cigarette smoking prevalence27, and implementation of MPOWER measures27,28, on country-level tobacco-related outcomes (e.g. prevalence of electronic cigarette use27; tobacco policy implementation28). Similar factors may be associated with market trends of MNCCs and FCCs.

Given these research gaps, the aims of this ecological study were to describe trends in global market shares of MNCCs and FCCs, and to assess associations with country-level factors across 78 countries from 2010 to 2020.

METHODS

Data sources and measures

Euromonitor passport market data

Market data come from Euromonitor Passport, an online database by the market research company Euromonitor International, which collects market data from several retail sources29. This dataset, has been previously used for tobacco control research30-32 and can serve to inform epidemiological surveillance. Data were available for 78 countries, none of which was low-income. Annual data collected between 2010 and 2020 for available countries obtained from Euromonitor included total retail volume (in million sticks) and percent market shares for FCCs (including menthol flavor) and MNCCs. The overall percent market shares of FCCs and MNCCs were calculated by Euromonitor as their respective proportions out of the total retail volume of cigarettes of all types (i.e. FCCs, MNCCs, standard cigarettes).

Country-level sociodemographic characteristics

Countries were categorized according to their geographical regions as defined by the WHO: African, Eastern Mediterranean, European, Americas, South-East Asia, and Western Pacific33. Income level classification also came from the World Bank and is based on Gross National Income (GNI) per capita (Atlas method, current US$) in 2020 (classified as of 1st July 2021, adjusted for inflation): low-income countries (<$1046), lower middle-income countries ($1046–4095), upper middle-income countries ($4096–12695), and high-income countries (>$12695)34.

The following sociodemographic data were also obtained from the World Bank: male and female population as percent of total population, male population aged 15-29 as percent of total male population, female population aged 15–29 years as percent of total female population, urban population as percent of total population, total unemployment as percent of total labor force. We derived the percent of population aged 15–29 years using the sum of female population aged 15–29 years and male population aged 15–29 years then divided by the total population. Gross Domestic Product (GDP) purchasing power parity (PPP) in international dollars per capita was obtained from the International Monetary Fund World Economic Outlook Database35. We derived GDP PPP in thousands of international dollars per capita by dividing by 1000.

Country-level smoking prevalence and MPOWER implementation

Country-level age-standardized estimates of cigarette smoking prevalence (as % of adult population aged ≥15 years) and data on country-level implementation of MPOWER were obtained from the WHO Global Health Observatory on Tobacco Control36. Data were available for the years 2010, 2012, 2014, 2016 and 2018, hence we used these to interpolate for the years 2011, 2013, 2015, 2017, and to extrapolate for 2019 and 2020. MPOWER measures include: Monitor tobacco use and prevention policies; Protect people from tobacco smoke; Offer help to quit tobacco use; Warn about the dangers of tobacco and anti-tobacco mass media campaigns; Enforce bans on tobacco advertising, promotion and sponsorship; and Raise taxes on tobacco. A score of 1 represents lack of data and scores 2–4 for M and 2–5 for POWER indicate increasing levels of implementation. A total MPOWER score was calculated by summing individual measure scores, ranging from a minimum of 6 (1 in each of the six measure scores) to a maximum of 29 (4 in M score and 5 in POWER scores)37.

Statistical analysis

Descriptive analyses

Country-level characteristics are presented as medians with interquartile range (IQR). We further present country-level mean values by WHO geographical region and World Bank country income groups. We derived retail volume per capita for the FCCs and MNCCs using the respective retail volume divided by the country’s total population size. We calculated annual growth rates (AGRs) in FCC and MNCC market shares for each country using the respective percent market shares from consecutive years, with the following formula for year n:

AGR values above 300% were capped at 300%, to avoid meaningless values resulting from an increase over a very small market share. We calculated average annual growth rates (AAGRs) of the FCC and MNCC market shares for each country were calculated as:

where N is the total number of years. We plotted country-level AAGR from 2010 to 2020 against percent market share for 2020 (or the latest available year) for FCCs and MNCCs, using bubble charts, with the size of the bubble representing the total cigarette retail volume.

Panel regression analysis

Linear fixed effects panel regression analyses were performed to evaluate the relationship between changes in country-level factors described above and changes in country-level percent market shares of FCCs and MNCCs, using Stata/SE 16.1. Fixed effects models were considered more appropriate than random effects models, as supported by the results of Hausman tests which showed a p<0.05. Also, fixed effects model controls for all time-invariant factors and therefore its estimated changes in market outcome will not be biased by the variation in time-invariant factors between countries. We examined predictor variables that have been found to be associated with FCC and MNCC use at the individual level, as well as country-level variables that have been associated with other tobacco-related outcomes5,12,18,22-25,27,28. Predictor variables were added into the model in incremental steps and no major changes in the magnitude or significance of coefficients were observed during this model fitting process. Presence of multicollinearity were examined by the variance inflation factor among predictor variables but was not identified. Regression coefficients (β) with 95% confidence intervals (CIs) for all predictor variables are presented.

RESULTS

Overall market trends of FCCs and MNCCs from 2010 to 2020

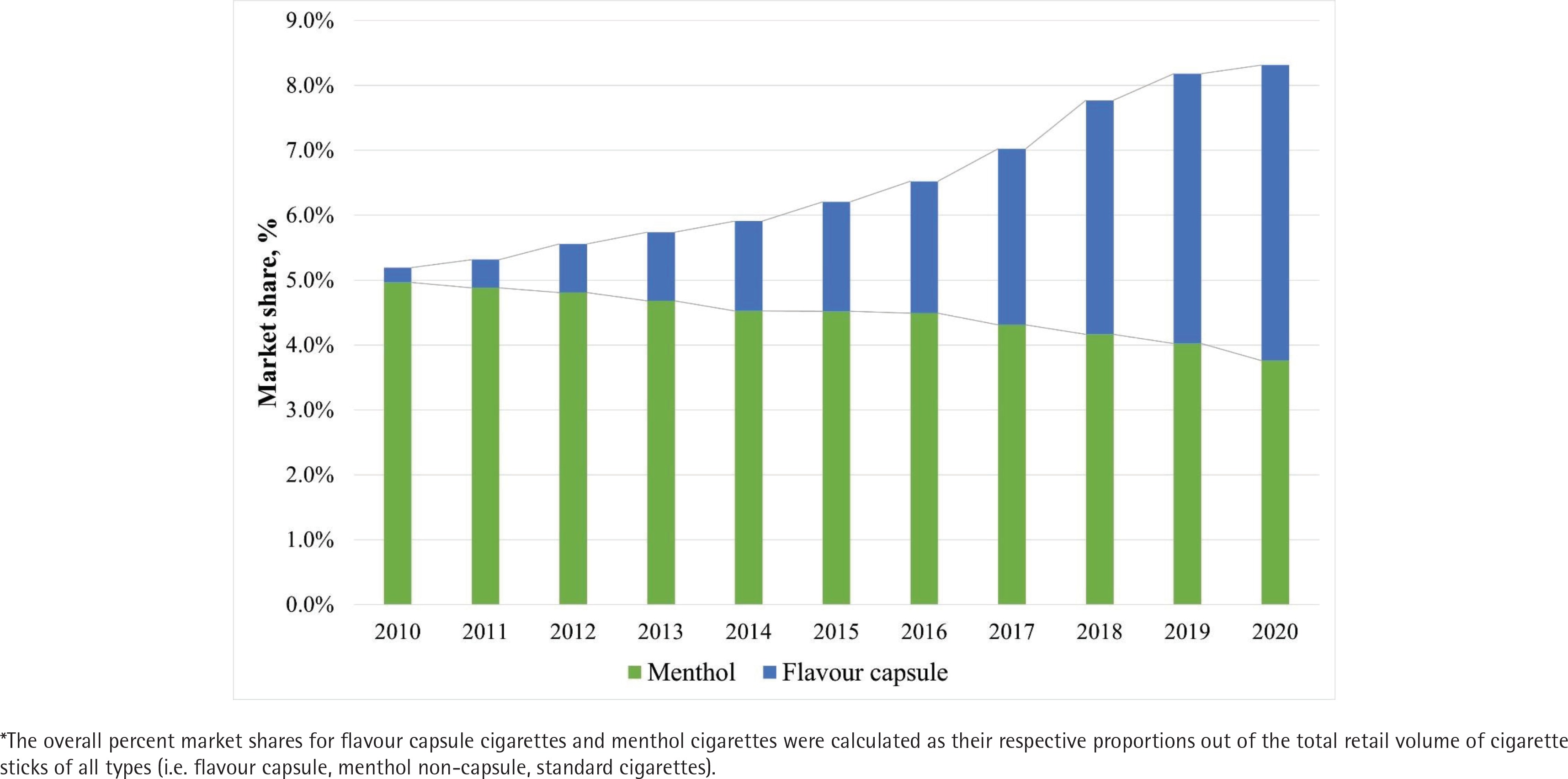

Medians with IQR of country-level characteristics and market outcomes in 2010 and in 2020 are presented in Table 1. The median percent market shares across countries for FCCs and MNCCs were 0.5% (IQR: 0.2–1.8; n=21 countries) and 4.1% (IQR: 1.7–10.6; n=78) in 2010 and 3.3% (IQR: 1.2–8.5, n=64) and 2.4% (IQR: 0.8–6.8; n=74) in 2020. The median retail volumes per capita of FCCs and MNCCs were 2.8 (IQR: 1.9–13.7) and 32.6 (IQR: 12.8–72.5) in 2010 and 18.7 (IQR: 4.7–48.9) and 14.6 (IQR: 4.0–33.7) in 2020. As depicted in Figure 1, the overall percent market share (i.e. total retail volume out of all cigarette types) increased from 0.2% in 2010 to 4.5% in 2020 for FCCs, surpassing MNCCs which decreased from 5.0% to 3.8% by 2019.

Table 1

Median values of country-level characteristics and market outcomes in 2010 and 2020

| 2010 | 2020 | |||||

|---|---|---|---|---|---|---|

| n | Median | IQR | n | Median | IQR | |

| Characteristics | ||||||

| Sociodemographic | ||||||

| Female population (% of total population)a | 77 | 50.7 | 50.0–51.3 | 77 | 50.6 | 50.0–51.3 |

| Population aged 15–29 years (% of total population)a | 77 | 22.5 | 19.6–27.4 | 77 | 19.2 | 16.8–23.7 |

| Urban population (% of total population)a | 77 | 68.9 | 55.2–80.9 | 77 | 73.7 | 57.7–82.7 |

| Unemployment rate (% of total work force)a | 77 | 7.3 | 4.8–10.0 | 77 | 6.2 | 4.7–9.3 |

| GDP per capita purchasing power parityb | ||||||

| (International dollars, in thousands) | 78 | 18.6 | 10.5–36.4 | 78 | 27.9 | 13.3–45.3 |

| Smokingc | ||||||

| Age-standardized prevalence of cigarette smoking (%)* | 71 | 23.5 | 16.2–28.7 | 71 | 19.8 | 12.0–25.3 |

| MPOWER overall score (range: 6–29) | 75 | 21.0 | 18.5–22.5 | 75 | 24.0 | 21.5–25.5 |

| Market outcomes by cigarette flavor categoryd | ||||||

| Flavored capsule cigarettes | 21 | 64 | ||||

| Market share (% retail volume) | 0.5 | 0.2–1.8 | 3.3 | 1.2–8.5 | ||

| Retail volume (in million sticks) | 84.6 | 15.4–264.9 | 228.2 | 69.4–2410.8 | ||

| Retail volume per capita | 2.8 | 1.9–13.7 | 18.7 | 4.7–48.9 | ||

| Menthol (non-capsule) cigarettes | 78 | 74 | ||||

| Market share (% retail volume) | 4.1 | 1.7–10.6 | 2.4 | 0.8–6.8 | ||

| Retail volume (in million sticks) | 597.8 | 185.6–1459.5 | 225.5 | 68.1–1014.2 | ||

| Retail volume per capita | 32.6 | 12.8–72.5 | 14.6 | 4.0–33.7 | ||

| Standard cigarettes | 78 | 78 | ||||

| Market share (% retail volume) | 95.7 | 89.4–98.3 | 93.4 | 79.9–98.0 | ||

| Retail volume (in million sticks) | 13668.7 | 5074.7–43301.4 | 9883.0 | 3689.0–30937.1 | ||

| Retail volume per capita | 903.9 | 451.8–1446.0 | 704.7 | 257.8–1055.5 | ||

| Total cigarettes | 78 | 78 | ||||

| Market share (% retail volume) | 100.0 | |||||

| Retail volume (in million sticks) | 14696.2 | 5098.3–46736.5 | 11238.5 | 3751.3–35801.5 | ||

| Retail volume per capita | 985.0 | 493.6–1532.4 | 751.6 | 366.6–1106.8 | ||

Market trends of FCCs by WHO region and country income level

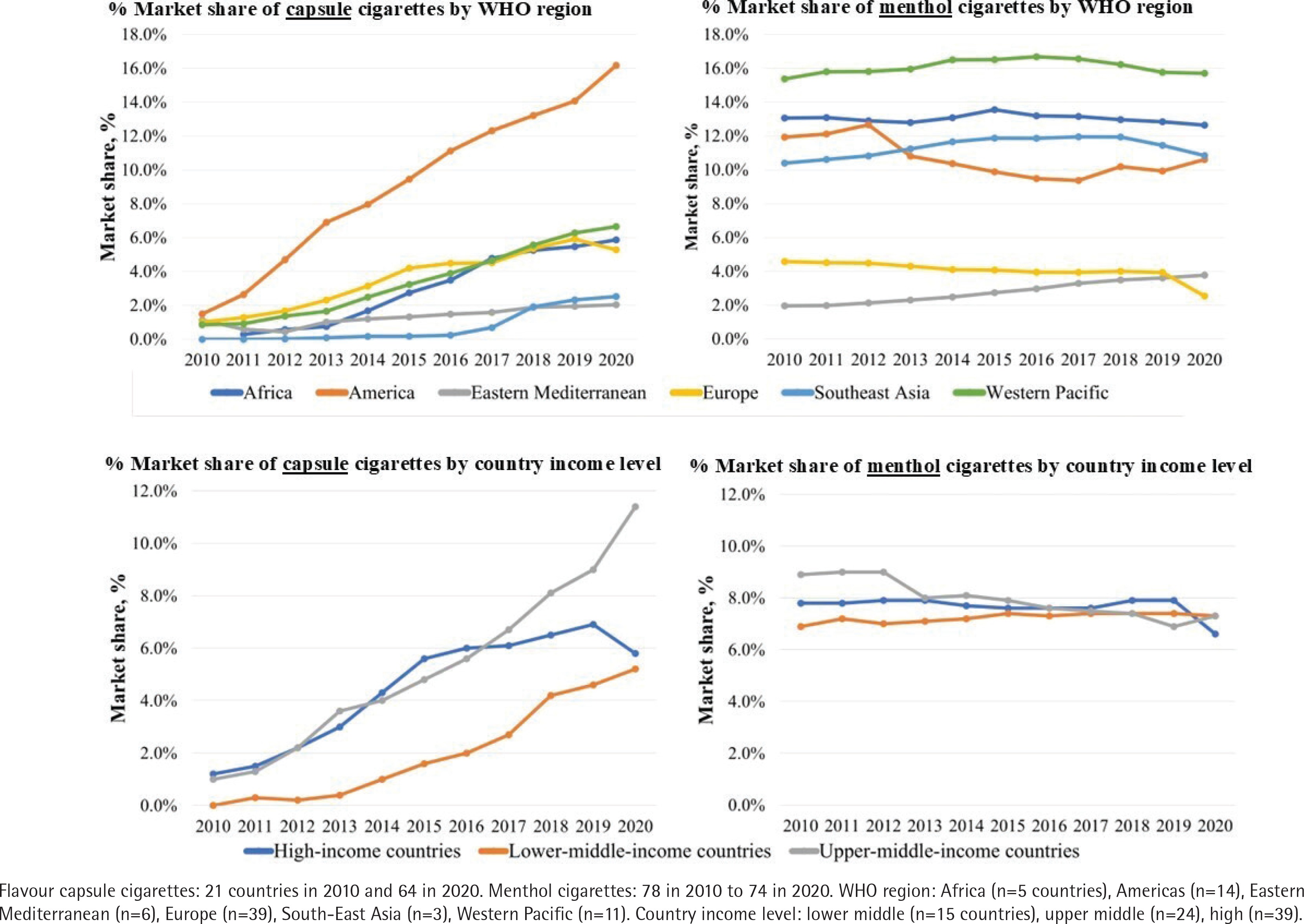

The average market share of FCCs generally increased across all WHO regions from 2010 to 2020, with the exception of Europe which saw an increase until 2019, followed by a decrease of 0.64 percentage points from 2019 to 2020 (Figure 2). Market increases in the region of the Americas were greater than other WHO regions (from 1.5% to 16.2%) (Table 2). This was mainly driven by the high market growth in Latin American countries, which made up four of the top five countries with the highest FCC market shares in 2020: Chile (48.4%), Peru (35.0%), Guatemala (32.6%), Mexico (27.3%), and South Korea (24.7%) (Table 3). There was an overall increase in FCC market share for lower middle-income, upper middle-income, and high-income country groups from 2010 to 2020 (Figure 2). The greatest increase was experienced by upper middle-income countries; on average each country’s market share increased by 9.93 percentage points during 2010–2020. These upward trends are further depicted in Supplementary file Figure 1, where the AAGR from 2010 to 2020 for FCCs was positive for the majority of countries (n=67), with the exception of five EU European countries. Four of the top five countries with highest AAGRs were lower and upper middle-income countries, three of which were non-EU European countries, including: India (154.1%), Uzbekistan (122.5%), Uruguay (114.8%), Russia (84.3%), and Ukraine (84.2%).

Table 2

Average market share (%) of flavor capsule cigarettes and menthol cigarettes from 2010 to 2020 by WHO region and country income level, Euromonitor Passport (for n countries in each region)

Table 3

Market share and average annual growth rate (AAGR) for flavor capsule cigarettes and menthol cigarettes by country (N=78), Euromonitor Passport 2010–2020

| Flavor capsule cigarettes | Menthol (non-capsule) cigarettes | |||||

|---|---|---|---|---|---|---|

| Country | WHO geographical region | World Bank country income level (2020) | % Market share* | % AAGR | % Market share* | % AAGR |

| Algeria | Africa | Lower middle | 0.6 | 5.9 | 0.4 | 5.0 |

| Argentina | Americas | Upper middle | 20.0 | 47.3 | 0.1 | -9.5 |

| Australia | Western Pacific | High | 2.7 | 6.5 | 6.8 | -0.7 |

| Austria | Europe | High | 1.5 | 30.5 | 0.2 | -19.3 |

| Azerbaijan | Europe | Upper middle | 5.8 | 33.0 | 2.2 | -7.1 |

| Belarus | Europe | Upper middle | 19.3 | 83.5 | 1.5 | 25.4 |

| Belgium | Europe | High | - | - | 1.9 | -6.3 |

| Bolivia | Americas | Lower middle | 1.6 | 61.3 | 5.2 | -1.0 |

| Bosnia and Herzegovina | Europe | Upper middle | 1.7 | 51.3 | 0.0 | 14.9 |

| Brazil | Americas | Upper middle | 3.9 | 57.0 | 2.8 | -12.2 |

| Bulgaria | Europe | Upper middle | 0.0 (2017) | -13.2 | 0.5 (2019) | -11.7 |

| Cameroon | Africa | Lower middle | 0.5 | 15.2 | 29.9 | 3.7 |

| Canada | Americas | High | - | - | 0.6 (2017) | -14.5 |

| Chile | Americas | High | 48.4 | 38.0 | 6.0 | 38.7 |

| China | Western Pacific | Upper middle | 2.8 | 73.6 | 0.1 | 2.9 |

| Colombia | Americas | Upper middle | 1.2 | 8.0 | 21.9 | 1.8 |

| Costa Rica | Americas | Upper middle | 18.2 | 26.5 | 1.0 (2019) | -11.2 |

| Croatia | Europe | High | 1.2 | 24.3 | 0.1 | -11.3 |

| Czech Republic | Europe | High | 3.6 (2017) | 17.4 | 6.5 | 5.0 |

| Denmark | Europe | High | 1.9 | 41.1 | 2.8 | -4.7 |

| Dominican Republic | Americas | Upper middle | 2.5 | 34.1 | 32.7 | 2.6 |

| Ecuador | Americas | Upper middle | 5.4 | 37.7 | 1.2 | -10.1 |

| Egypt | Eastern Mediterranean | Lower middle | 2.3 | 67.4 | 0.0 | 6.3 |

| Estonia | Europe | High | 0.4 | 19.7 | 0.4 | -16.2 |

| Finland | Europe | High | 6.0 (2016) | 35.4 | 5.8 | -9.6 |

| France | Europe | High | 3.6 (2016) | 70.4 | 1.4 | -7.8 |

| Georgia | Europe | Upper middle | 2.6 | 13.2 | 3.2 | -2.6 |

| Germany | Europe | High | - | - | 0.8 | -5.8 |

| Greece | Europe | High | 0.2 | 7.8 | 0.1 | 17.4 |

| Guatemala | Americas | Upper middle | 32.6 | 37.7 | 9.6 | -4.1 |

| Hong Kong | Western Pacific | High | 13.3 | 81.2 | 27.3 | -0.2 |

| Hungary | Europe | High | 12.1 (2017) | 52.5 | 8.1 | 6.7 |

| India | South-East Asia | Lower middle | 6.3 | 154.1 | 0.8 | 6.2 |

| Indonesia | South-East Asia | Lower middle | 0.5 | 60.0 | 4.4 | 10.0 |

| Ireland | Europe | High | 1.3 | 48.4 | 0.0 | -16.4 |

| Israel | Europe | High | 0.0 | 41.8 | 1.0 | -6.2 |

| Italy | Europe | High | 0.0 | -8.2 | 0.1 | -10.1 |

| Japan | Western Pacific | High | 7.0 | 15.9 | 27.7 | 2.9 |

| Kazakhstan | Europe | Upper middle | 16.8 | 54.6 | 0.7 | -15.3 |

| Kenya | Africa | Lower middle | 0.5 | 6.4 | 5.9 | 2.8 |

| Latvia | Europe | High | 4.7 | -0.2 | 1.5 | -2.9 |

| Lithuania | Europe | High | 3.9 | 29.3 | 3.9 | -1.0 |

| Malaysia | Western Pacific | Upper middle | 0.7 | 20.5 | 24.8 | 1.3 |

| Mexico | Americas | Upper middle | 27.3 | 13.0 | 0.4 | -26.4 |

| Morocco | Eastern Mediterranean | Lower middle | 0.6 | 14.1 | 4.2 | 3.7 |

| Netherlands | Europe | High | 0.6 (2017) | 12.8 | 1.4 | -10.1 |

| New Zealand | Western Pacific | High | 4.7 | 48.7 | 9.6 | -1.0 |

| Nigeria | Africa | Lower middle | 18.7 | 75.5 | 24.1 | -2.4 |

| North Macedonia | Europe | Upper middle | - | - | 0.0 | 0.9 |

| Norway | Europe | High | 6.4 | 14.1 | 9.1 | -0.6 |

| Pakistan | Eastern Mediterranean | Lower middle | - | - | 2.7 | 2.1 |

| Peru | Americas | Upper middle | 35.0 | 39.2 | 18.0 | -2.3 |

| Philippines | Western Pacific | Lower middle | 4.6 | 11.4 | 22.6 | -0.4 |

| Poland | Europe | High | 7.7 | 14.2 | 20.6 | 3.1 |

| Portugal | Europe | High | 6.2 | 13.5 | 2.1 | -4.4 |

| Romania | Europe | Upper middle | 1.9 (2019) | -1.9 | 2.0 | -10.3 |

| Russia | Europe | Upper middle | 22.9 | 84.3 | 1.8 | -6.0 |

| Saudi Arabia | Eastern Mediterranean | High | 3.4 | 11.9 | 12.4 | 18.9 |

| Serbia | Europe | Upper middle | 0.2 | 19.9 | 0.2 | -2.1 |

| Singapore | Western Pacific | High | 3.2 | 41.2 | 47.5 | 0.1 |

| Slovakia | Europe | High | 2.9 | 45.1 | 1.0 | -17.7 |

| Slovenia | Europe | High | 1.3 | -6.8 | 0.7 | -7.8 |

| South Africa | Africa | Upper middle | 9.0 | 36.9 | 2.9 | -9.7 |

| South Korea | Western Pacific | High | 24.7 | 60.6 | 2.8 | -4.7 |

| Spain | Europe | High | 0.3 | 21.7 | 0.0 | -21.3 |

| Sweden | Europe | High | 1.8 | 50.0 | 4.2 | -10.2 |

| Switzerland | Europe | High | 1.8 | 31.0 | 2.4 | 2.1 |

| Taiwan | Western Pacific | High | 8.3 | 61.7 | 1.2 | 2.9 |

| Thailand | South-East Asia | Upper middle | 0.8 | 10.9 | 27.3 | -0.5 |

| Tunisia | Eastern Mediterranean | Lower middle | - | - | 3.3 | -1.3 |

| Turkey | Europe | Upper middle | 0.8 (2019) | 38.4 | 0.3 (2019) | -12.4 |

| Ukraine | Europe | Lower middle | 14.8 | 84.2 | 2.2 | 17.3 |

| United Arab | Eastern Mediterranean | High | 1.9 | 49.8 | 0.1 | -10.6 |

| Emirates | ||||||

| United Kingdom | Europe | High | 4.6 | 69.8 | 2.4 | -6.3 |

| Uruguay | Americas | High | 8.7 | 114.8 | 0.0 | -8.9 |

| USA | Americas | High | 5.5 | 12.3 | 29.5 | 0.0 |

| Uzbekistan | Europe | Lower middle | 15.7 | 122.5 | 1.8 | -5.6 |

| Vietnam | Western Pacific | Lower middle | 1.2 | 49.4 | 2.4 | 5.5 |

Market trends of MNCCs by WHO region and country income level

In contrast, average market shares for MNCCs remained relatively stable from 2010 to 2020 in WHO regions with the highest market shares: Western Pacific (15.4% to 15.7%), Africa (13.1% to 12.6%), Americas (11.9% to 10.6%), and South-East Asia (10.4% and 10.8%) (Figure 2 and Table 2). Average MNCC market shares in the Eastern Mediterranean were comparatively lower, however, they experienced growth from 2.0% in 2010 to 3.8% in 2020, while in Europe market shares decreased over time, with the largest decline from 2019 to 2020. Average market share of MNCCs did not vary by country income level. The five highest MNCC markets in terms of market share in 2020 were: Singapore (47.5%), Dominican Republic (32.7%), Cameroon (29.9%), USA (29.5%), and Japan (27.7%) (Table 3). The majority of countries (n=50) had a negative AAGR for MNCCs (Supplementary file Figure 1). Countries with the highest AAGR included: Chile (38.7%), Belarus (25.4%), Saudi Arabia (18.9%), Greece (17.4%) and Ukraine (17.3%) (Table 3).

Country-level factors associated with FCC and MNCC market shares

Associations between country-level factors and average percent market shares of FCCs and MNCCs are presented in Table 4. Market share of FCCs increased on average by 0.68 percentage points (95% CI: 0.38 – 0.98) per year from 2010 to 2020 (p<0.001). The following factors were negatively associated with market share of FCCs: percent of the population aged 15–29 years (β= -0.57; 95% CI: -0.98 – -0.15, p=0.008), percent of urban population (β= -0.88; 95% CI: -1.28 – -0.48, p<0.001), GDP PPP per capita (β= -0.13; 95% CI: -0.24 – -0.03, p=0.015), and age-standardized prevalence of cigarette smoking (β= -0.93; 95% CI: -1.38 – -0.49, p<0.001). Unemployment rate was positively associated with market share of FCCs (β=0.28; 95% CI: 0.12–0.44, p=0.001), but no significant association was observed with percent female population and overall MPOWER score.

Table 4

Country-level factors associated with average percent market share of flavor capsule cigarettes and menthol cigarettes, from 2010 to 2020, Euromonitor Passport

| Factors | Flavor capsule | Menthol (non-capsule) | ||||

|---|---|---|---|---|---|---|

| β* | 95% CI | p | β* | 95% CI | p | |

| Year | 0.68 | 0.38 – 0.98 | <0.001 | -0.19 | -0.31 – -0.06 | 0.003 |

| Female population (% of total population) | 0.34 | -0.73 – 1.41 | 0.530 | -0.16 | -0.63 – 0.31 | 0.512 |

| Population aged 15–29 years (% of total population) | -0.57 | -0.98 – -0.15 | 0.008 | -0.07 | -0.23 – 0.10 | 0.439 |

| Urban population (% of total population) | -0.88 | -1.28 – -0.48 | <0.001 | 0.24 | 0.08 – 0.40 | 0.003 |

| Unemployment rate (% of total work force) | 0.28 | 0.12 – 0.44 | 0.001 | -0.09 | -0.17 – -0.02 | 0.014 |

| GDP PPP per capita (international dollars, in thousands) | -0.13 | -0.24 – -0.03 | 0.015 | -0.03 | -0.08 – 0.01 | 0.160 |

| Age-standardized prevalence of cigarette smoking | -0.93 | -1.38 – -0.49 | <0.001 | -0.14 | -0.31 – 0.04 | 0.124 |

| Overall MPOWER score | 0.04 | -0.17 – 0.25 | 0.728 | -0.07 | -0.16 – 0.03 | 0.173 |

In contrast, market share of MNCCs decreased on average by 0.19 percentage points (95% CI: -0.31 – -0.06) per year from 2010 to 2020 (p=0.003). The percent of urban population was positively associated with market share of MNCCs (β=0.24; 95% CI: 0.08–0.40, p=0.003), while unemployment rate was negatively associated with market share of MNCCs (β= -0.09; 95% CI: -0.17 – -0.02, p=0.014). No other associations were statistically significant.

DISCUSSION

This study of data from 78 countries found that between 2010 and 2020, global market share of FCCs (including menthol flavor) increased by an average of 0.7% per year, while MNCC share slightly decreased by an average of -0.2% per year. As of 2019, the overall cigarette market share of FCCs surpassed that of MNCCs. The largest increases in FCCs were observed among upper middle-income countries and countries in the WHO Americas region. Average market share of MNCCs remained highest in the WHO Western Pacific and Africa regions. After adjusting for country-level factors, market share of FCCs was positively associated with unemployment rate and negatively associated with percent population aged 15–29 years, percent urban population, GDP PPP, and smoking prevalence. In contrast, the MNCC market share was negatively associated with unemployment rate and positively associated with percent urban population. Neither FCC nor MNCC market shares were associated with percent of female population or overall MPOWER score.

Results from this study add to previous evidence that FCCs have expanded quickly in the past decade11,19, with growth continuing as of 2020. Unlike previous studies that have only focused on market share, we also examined retail volume per capita and AAGR, which provide a more nuanced view of FCC trends. While the overall global market share of MNCCs decreased slightly from 2010 to 2020, trends were relatively stable across all WHO regions and country income groups. The overall global decline may not reflect actual reductions in MNCC use because many FCCs are mentholated, and in some countries exclusively so20. A study in the US found that while MNCC consumption declined from 2008 to 2020, menthol FCC consumption increased38. While this differentiation could not be assessed in the current study, our findings nevertheless indicate a lack of progress in reducing menthol use over the past two decades, particularly among countries with the highest MNCC market shares. Data from 2001 show that the countries among the top five leading MNCC markets included Singapore, Cameroon, and the USA, which continued to be the case in our study in 202018. This is disconcerting given the well-established evidence of the role of menthol in increasing appeal of cigarettes and facilitating smoking initiation and progression to regular use6,7.

While an increasing number of countries have adopted flavor cigarette bans39, in line with the WHO FCTC Article 9 recommendation to prohibit or restrict ingredients, including flavors40, implementation of this measure remains subpar3. This, coupled with industry marketing strategies is likely allowing for global market growth of flavored tobacco products12,41. The notable market decreases in FCCs and MNCCs in the WHO Europe region from 2019 and 2020 may be partly attributable to implementation of the EU ban on characterizing flavors in cigarettes, which took effect in May 2017, with the exception of menthol, which had a grace period until May 2020.

Our finding, that overall MPOWER scores were not associated with either FCC or MNCC subpar market shares, may at least in part be due to the fact that these measures do not account for implementation of WHO FCTC Article 9 on regulating the content of tobacco products. Moreover, the rise in flavored tobacco products has occurred even in some countries with the highest levels of WHO FCTC implementation, such as in Latin America42. However, to date no Latin American country has successfully implemented a ban on MNCCs43. While Brazil was the first country worldwide to adopt a ban on all flavor additives, including menthol, in 2012, policy implementation continues to be held up by tobacco industry litigation44. Many Latin American countries have also experienced a decrease in the overall smoking prevalence of cigarettes over time42, which may explain the inverse association found between smoking prevalence and FCC market share. It is possible that the tobacco industry is concentrating efforts where smoking prevalence is declining to increase product use. There is also evidence that the tobacco industry has used innovations such as FCCs as a marketing strategy to drive sales, particularly in light of marketing restrictions and other tobacco control policies4,12. For instance, adoption of standardized packaging legislation in Australia, Singapore and the UK was followed by the introduction of several new FCC products to the market12,45-47. It is therefore not surprising that FCCs are often marketed using less regulated avenues, such as advertising at the point-of-sale and the use of packaging, which has particularly been observed in Latin American countries and in low- and middle-income countries, which as indicated in our study is where FCC use is highest12,21. In many Latin American countries, retail availability of FCCs, often near schools, is ubiquitous48-51.

The rapid rise of these products is alarming given that FCCs are particularly popular among youth and young adults, as well as females in many countries11,19,20,23. However, we found that at a country level, market trends were not associated with the percent of population that are female and were in fact inversely associated with the percent of young people aged 15–29 years in the population. At an ecological level, these factors may not change enough over time to explain trends in market shares. Our additional findings that unemployment rate, urbanicity, GDP PPP per capita were associated with the MNCC and/or FCC market share may explain factors driving market variations of these products across different countries. It is also plausible though that growth of these products in some regions over others was not primarily driven by country-level characteristics, but rather a by-product of tobacco industry marketing priorities. While market share of FCCs was positively associated with unemployment rate and negatively associated with percent urban population, the inverse was found for the MNCC market share, which may be reflective of different industry marketing strategies for the respective products.

Strengths and limitations

There are limitations of this study that must be considered. Euromonitor International has been collaborating with the tobacco industry in recent years. We do not have reason to believe that this affected the quality of market data that we have used, unlike other types of data (e.g. illicit trade), although their methodology was not documented in detail52,53. The absence of data from low-income countries limits generalizability of findings, particularly in analyses assessing associations between country income level and market outcomes. However, the included countries had a combined population of 6.21 billion in 2020, accounting for 80.1% of the world population. In addition, we interpolated and extrapolated years of data for prevalence of cigarette smoking and MPOWER measures in order to preserve granularity in the annual market outcomes obtained, which may have attenuated associations between variables. In this study, FCCs and MNCCs were examined as separate categories. However, many capsule cigarettes are menthol flavored and therefore the market of MNCCs may be underestimated in these analyses. Despite these limitations, this study is strengthened by the ability to compare across a large number of countries, particularly in light of the scarce data on global prevalence of flavored cigarette use12. Moreover, our study offers new insight on which country-level factors may be in part driving growth of FCCs and MNCCs and/or which country-level factors may be targeted by the tobacco industry in its marketing efforts.

CONCLUSIONS

This study provides a global snapshot of the market landscape of flavor capsule cigarettes (FCCs) and menthol (non-capsule) cigarettes (MNCCs). We found that FCCs have experienced substantial growth, particularly among countries of the WHO Americas region and in upper middle-income countries, from 2010 to 2020. The overall market share of MNCCs slightly decreased, but remained high in many countries, with the highest shares in the WHO Western Pacific and Africa regions. By 2019, FCCs made up a larger proportion of the global cigarette market than MNCCs. Country-level factors associated with market shares of FCCs and/or MNCCs, such as smoking prevalence, unemployment rate, and urbanicity, found in this study, may be associated with popularity of these products in some countries versus others. Policymakers should be aware of these factors that may contribute to higher market shares of these products. Moreover, given that these country characteristics may also be indicative of tobacco industry’s marketing efforts and priorities, tobacco industry activity should also be closely monitored. Findings support the critical need for increased efforts to address flavors and innovative features used in tobacco products. These data can be used by advocates and policy makers to monitor and support implementation of measures to curb growth of flavored cigarettes. Given the scant global epidemiological data on prevalence of flavored tobacco products, future research should prioritize population-level studies for more comprehensive surveillance, particularly in priority countries and regions identified in this study.